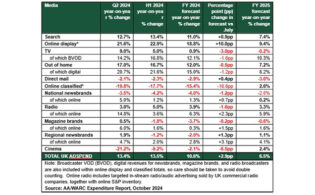

The U.K. advertising market avoided a contraction in Q2 thanks to growth in online formats and BVOD, according to the latest Advertising Association/WARC Expenditure Report.

In line with previous forecasts, the U.K. ad market grew by 1 percent in the second quarter to reach almost £9 billion ($10.9 billion). While TV was down 12.8 percent, BVOD showed a 5.6 percent increase.

For the year, AA/WARC projects total adspend will be up 2.6 percent to £35.6 billion ($43.2 billion), with TV down 5.8 percent but BVOD up 16.1 percent. Sporting events such as the FIFA Women’s World Cup and the Rugby World Cup, plus the return of Big Brother to ITV and the success of the Barbie and Oppenheimer films, are expected to lift the market despite the economic headwinds.

Looking ahead to 2024, AA/WARC anticipates a gain of almost 4 percent to reach £37 billion ($44.9 billion).

Stephen Woodford, CEO of the Advertising Association, noted: “Advertising continues to show itself as a weather vane for the U.K. economy, with the advertising market expected to grow slightly more than the economy, with both barely in positive figures. Looking ahead to 2024, we expect to see more channels experience growth again, as the ad market grows to £37 billion for the year. As we anticipate the General Election next year, the Advertising Association will continue to demonstrate advertising’s contribution to a strong economy, not least that brands that continue to invest in advertising during a downturn are more likely to post better returns when emerging from tough conditions.”

James McDonald, director of data, intelligence and forecasting at WARC, added: “The U.K.’s economy continues to skirt with recession as households make cutbacks in the face of stubbornly high inflation, and unemployment slowly ticks upwards as activity in the private sector cools. It is therefore encouraging that, amid this backdrop, the U.K.’s advertising industry was able to grow during the first six months of 2023 and that the market is on course to be 2.6 percent larger this year overall. It should, however, be noted that this growth is concentrated in certain corners of the industry, with broadcasters and publishers bearing the brunt of an unfavorable trading climate, while digitally native platforms largely prosper.”